Hello! This is LUMOS, the automated financial management solution for government-funded projects.

For early-stage startups or R&D-focused technology firms, government grants and project funds represent an unparalleled channel for securing capital. Unlike bank loans, they do not carry interest expenses; unlike venture capital investment, they do not require exhaustive, months-long processes to close. However, unlike debt or investments, government funding must be utilized strictly in accordance with established rules and guidelines. Most importantly, failure to comply with these rules can result in a requirement to return the funds after the project concludes.

So, who evaluates whether the funds were spent in compliance with the guidelines? That responsibility falls to Certified Public Accountants (CPAs). Once the project is complete, a CPA determines whether the expenditures complied with the rules through a formal financial audit. Today, we will explore the three primary criteria that CPAs utilize when conducting financial audits of your project funding.

Risk Assessment

The risk assessment is the stage where auditors measure the audit risk of the subject (the project budget execution details) before beginning the formal financial audit. Based on the assessed risk level, they determine the nature, scope, and time allocated for the audit procedures. Simply put, prior to auditing, the auditor evaluates the probability of errors or irregularities in how the funds were managed and plans the depth of the audit accordingly.

In other words, before performing the audit, the CPA analyzes the fund allocation categories, the frequency of budget revisions, and any history of non-compliance found during pre-checks to estimate the likelihood of errors and determine the time required for the engagement.

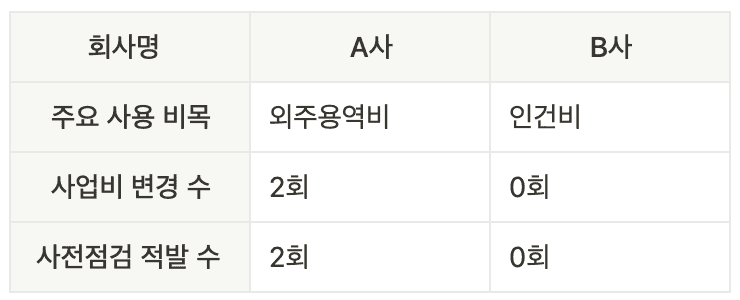

Let us assume an example of two companies, Company A and Company B.

The CPA in charge of auditing both companies would likely assess Company A as having a higher audit risk than Company B. Outsourced services generally require a larger volume of templates and supporting documentation than regular labor costs, and they involve more subjective judgment regarding project relevance. Additionally, Company A had higher frequencies of budget revisions and was flagged during pre-checks. For these reasons, the CPA concludes that Company A has a higher probability of accounting discrepancies than Company B.

Audit Time Allocation

Based on the risk assessment, the CPA determines the hours dedicated to the audit. Areas designated as high-risk receive more thorough examination, while lower-risk areas require less time. This is referred to as "audit time allocation." In the case of Company A, the CPA will spend significantly more time reviewing templates and supporting documentation; conversely, Company B's audit will be completed in relatively fewer hours.

Consequently, if your organization falls into a higher audit risk category, dedicating extra diligence to preparing templates and supporting documentation after spending funds is crucial to mitigating the risk of disallowed expenses.

Professional Skepticism

When performing an audit, CPAs approach their work with two fundamental mindsets: a questioning mind and a critical assessment of audit evidence. Put simply, they do not accept submitted templates and documentation at face value. This professional attitude is known as "professional skepticism."

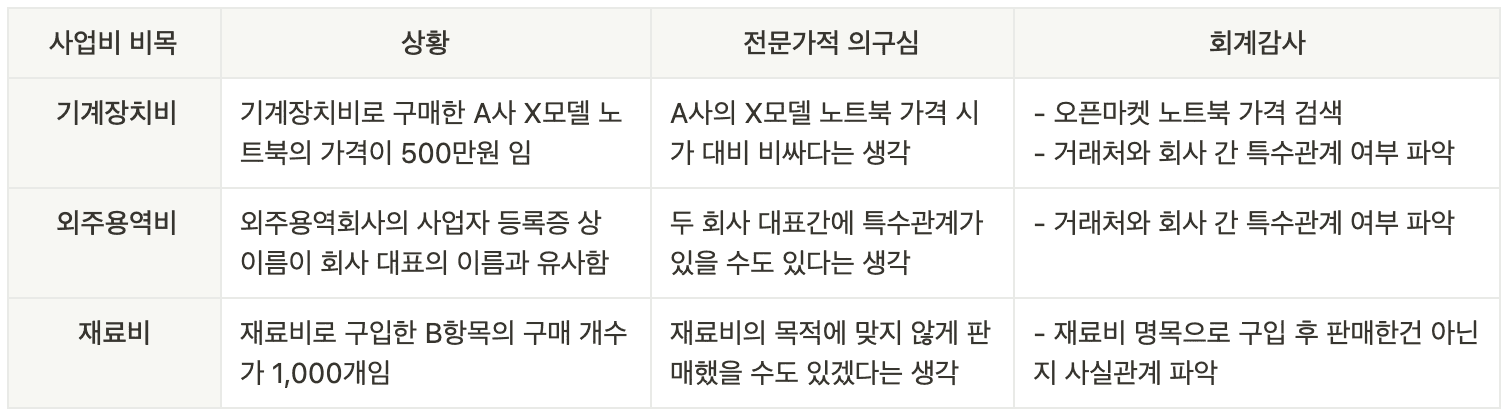

Professional skepticism is rigorously applied during audits of government-funded projects, as shown in the examples below.

As demonstrated, auditors evaluate all submitted records and proof with professional skepticism. This critical evaluation informs their risk assessment and ultimately dictates the time allocated to the audit.

Today, we have briefly examined how CPAs approach audits of government-funded projects. Understanding the financial audit process—the final hurdle of project funding—will help alleviate concerns about disallowed expenses and ensure solid compliance during the course of the project.