Hello! We are LUMOS, the automated expense management solution for government-funded projects.

Expense rules for government funding can be highly complex. This is because these rules are legally grounded in various statutes, such as the National Research and Development Innovation Act and the Support for Small and Medium Enterprise Startups Act. Furthermore, the official manuals designed to help interpret these complex laws often span hundreds of pages, making them difficult to understand for standard project investigators who are not legal experts. However, because government-funded projects utilize public fiscal resources, establishing strict rules through legislation is necessary to ensure transparency and fairness.

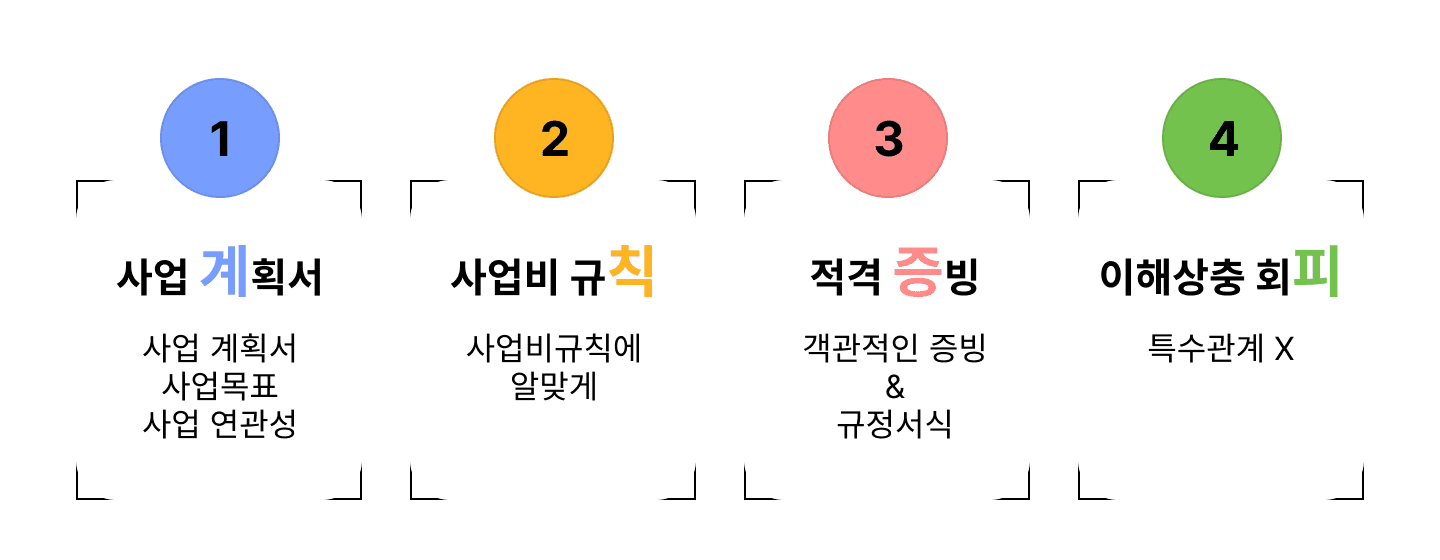

Even within these complex rules, there is logical consistency. Today, we will simplify these challenging expense regulations. You only need to remember four core principles: Plan, Rule, Proof, and Conflict. Let's look at these four principles!

“Plan” – The Project Proposal

The first principle of funding expenses is the "Project Proposal," which establishes project relevance. Government-funded projects receive financial support specifically to achieve the goals outlined in the project or research proposal. Naturally, project funds must be used exclusively for the work specified in that proposal.

Even if an expense is otherwise compliant with general rules, it will be disallowed if it bears no relevance to your specific project or research. What qualifies as project-relevant? Because this varies significantly by task and program, there is no single universal standard. However, expenses pre-registered in the execution plan of the project proposal are approved through the agreement, meaning they are officially recognized as project-relevant.

“Rule” – Regulatory Compliance

The second principle is executing funds in strict compliance with regulations. While this may sound obvious, it is important to address how these rules must be interpreted.

Government funding regulations are rooted in law, meaning they must be interpreted literally. Unless the rules provide explicit exceptions, you must not choose a broad interpretation of the written text. For example, if a rule states "The representative's labor costs must be calculated as an in-kind contribution," then in the absence of other specifications, co-representatives must also be interpreted simply as "representatives."

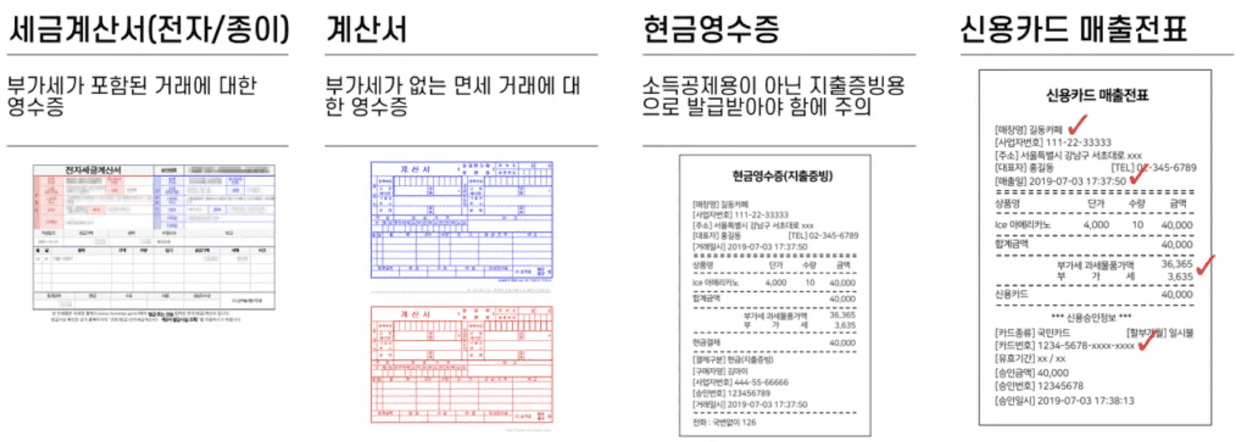

“Proof” – Qualified Documentation

Unlike general corporate funds, government project funds must be thoroughly accounted for after use. This proof must be provided through legally "qualified documentation" under tax law. Qualified documentation typically includes the following:

Under funding regulations, qualified tax documentation must be obtained for all expenses (excluding specific exceptions, such as certain labor or mentoring fees). This is necessary to prove that the company has actually executed the payment. Consequently, transactions between individuals where qualified documentation cannot be issued are not permitted.

“Conflict” – Avoiding Conflicts of Interest

Government project funds cannot be paid to "specially related parties." Allowing transactions with related parties introduces the risk of arbitrary price manipulation and potential misappropriation of funds. In this context, related parties generally refer to those defined under civil and tax law. To put it simply, this includes relatives, as well as companies with which you have had an employment relationship within the past two years.

Today, we explored the four essential principles of government-funded project expenses. Keeping these four factors—Plan, Rule, Proof, and Conflict—in mind will serve as a valuable guide whenever you need to determine whether a specific expense or vendor is compliant.