Hello!

We are LUMOS, the automated management solution for government-funded R&D business expenses.

Previously, we covered the steps and procedures for the TIPS program. In this session, we will introduce several essential terminology commonly used in government-funded programs, particularly R&D support initiatives like TIPS. Just as we learned about the organizational and executing bodies (such as specialized and managing agencies) in our last session on structural systems, this post will discuss key financial terms you must know regarding the utilization of R&D funds.

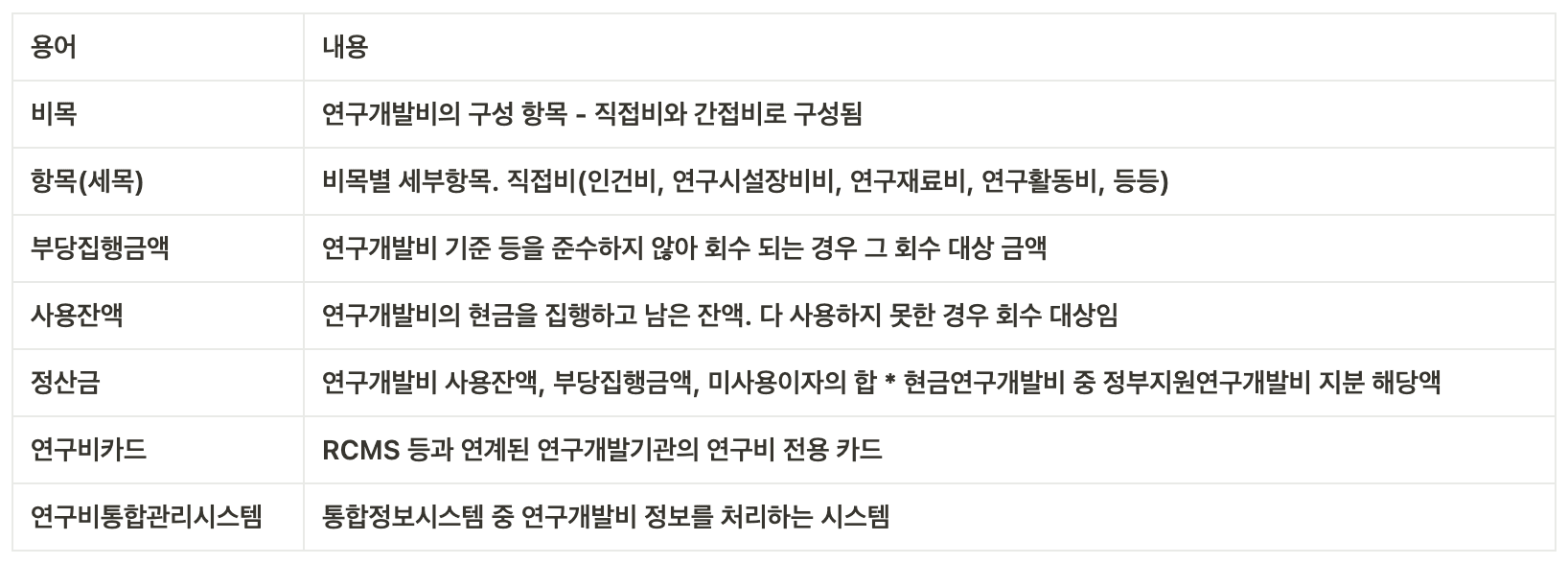

Basic Terminology

These are the foundational terms and explanations required for managing R&D business expenses (research funds). Since these definitions apply to all national R&D projects governed by the National Research and Development Innovation Act, we highly recommend that organizations starting their very first research project via the TIPS program familiarize themselves with these terms.

Among the basic terminology, "settlement balance" (reconciliation amount) is particularly important. After a research project is completed, only the portion corresponding to the government-funded share out of the total remaining balance, ineligible expenditures, and unused interest is calculated and returned. In other words, you do not need to reconcile or return the cash portion originally contributed by the participating organization at the start of the project.

Government Contributions vs. Matching Funds (Organizational Share)

When executing TIPS, you do not rely solely on government R&D funding; the performing organization (the TIPS recipient) must also contribute a matching portion of the total budget. This matching contribution is referred to as the "organizational share."

In the case of the TIPS program, the performing organization must contribute at least 20% of the total R&D budget. For example, if the government contribution is 500 million KRW and the matching organizational contribution is 125 million KRW, the total R&D budget equals 625 million KRW. Here, the organizational share of 125 million KRW divided by the total 625 million KRW correctly meets the 20% minimum requirement.

Cash Contributions vs. In-Kind Contributions

Within the organizational share, it is essential to distinguish between "cash" and "in-kind" contributions. The organizational share generally refers to the budget deposited or allocated by the performing (commercial) entity corresponding to the government grant. However, cash and in-kind contributions differ in the following ways:

Cash: The specific portion of the matching contribution that the TIPS performing organization must directly deposit in cash into the designated R&D account.

In-kind: The non-monetary value or committed resources that the TIPS performing organization agrees to contribute and consume as part of the project expenses.

In short, the cash portion must actually be transferred to the dedicated R&D bank account. For in-kind contributions, since they represent committed resources (such as labor costs) the TIPS organization agrees to consume, the performing entity must actually utilize and prove those expenses during the project cycle. Please note that if in-kind contributions are not consumed or fall short of the committed amount, the difference must be paid back in cash upon the completion of the TIPS project.

For in-kind contributions, most TIPS performing companies allocate them toward the representative's or founder's labor costs. In doing so, careful attention is required to ensure no deficit occurs in the in-kind labor budget. To assist you, LUMOS, the automated management solution for government-funded R&D expenses, provides alert and reminder features to help you track in-kind labor costs effortlessly.

Today, we explored the essential terms and concepts required when executing the TIPS program. These definitions will prove highly useful for all future R&D projects beyond TIPS, so we encourage you to keep them in mind.

We will return in our next post with more detailed guidance on managing your TIPS R&D funds effectively.