Hello!

We are LUMOS, the automated management solution for government-funded R&D project expenses!

Previously, before diving into the TIPS expense regulations, we covered the governance and structure of the TIPS program. In this session, we will explore the procedural steps of TIPS. Understanding the entire sequence of procedures is crucial for TIPS expense management. Knowing the milestone events—from selection and receiving funding to evaluation and financial audits—enables more efficient and effective expense management.

In this post, we will divide the progress into three main stages: Pre-selection, Mid-project, and Post-completion, and discuss the key considerations for each stage.

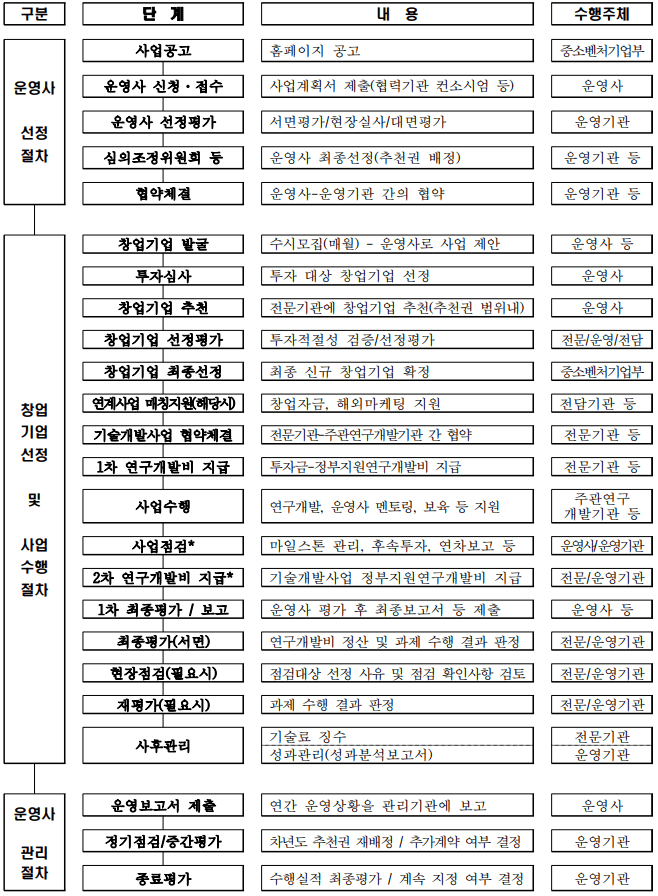

<TIPS Overall Process>

Pre-selection

Checking the Number of Projects and Personnel Labor Cost Allocation Rates

Numerous government-funded R&D projects are announced every year, but companies cannot participate in an unlimited number of them. By law, Korea limits the number of national R&D projects a researcher can concurrently perform. This is known as the "3-Project, 5-Participation" (3-Chaek, 5-Gong) rule.

The "3-Project, 5-Participation" rule means that a person can serve as a Principal Investigator (PI) for up to 3 projects, and participate as a researcher (including co-investigator) in up to 5 projects simultaneously.

Consequently, if the representative of the TIPS-performing company (acting as the PI) is already serving as the PI for three other projects, they cannot participate in TIPS. Similarly, if an employee to be registered as a researcher under the TIPS project is already participating in five other projects, they cannot be added.

However, projects scheduled to end within six months from the deadline of the proposal submission are excluded from this limit.

Additionally, the labor cost allocation rate for any researcher cannot exceed 100% when combined across all participating projects.

Mid-project

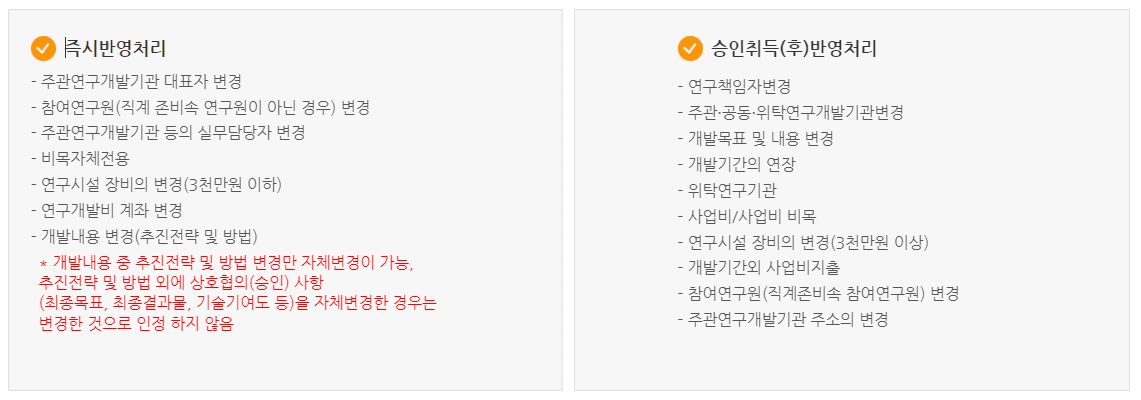

Agreement Modifications

During project execution, various changes often require modifications to the original agreement. Expense restructuring is one of the most common reasons. Agreement modifications are classified into minor modifications (simple notification) and major modifications (requiring approval). For simple notifications, the performing company only needs to update the online system. In contrast, modifications requiring approval must be formally reviewed and approved by the officer in charge.

Examples of Modification Types

Transitioning from Year 1 to Year 2

TIPS is executed over a total of two years, divided into Year 1 and Year 2. An interim evaluation is conducted at the end of the first year, alongside an annual progress report and financial audit. Year 2 can only proceed if the project receives a "Continue" rating from the Year 1 evaluation.

At this stage, unused funds from Year 1 can be carried over to Year 2 through a formal carryover application. Note that once Year 1 funds are carried over into the Year 2 budget, those specific carried-over funds cannot subject to further budget category reallocations.

Therefore, when applying for budget carryover at the end of Year 1, careful planning is required to ensure these funds can be utilized exactly as designated for Year 2.

Post-completion

R&D Expense Usage Reporting and Audit Support

The primary lead organization must submit the R&D expense usage report, an independent accountant's audit report, and supporting documentation online within three months of the project completion date.

Financial audits begin after the project concludes. During this period, organizations face an influx of requests for receipts, invoices, and factual clarifications regarding previous transactions.

Many TIPS-performing companies only begin organizing their records once the actual financial audit starts. This often leads to issues with missing documentation and difficulty recalling specific transaction details.

However, companies utilizing the automated expense management solution LUMOS can maintain systematic history and transaction records throughout the project, enabling a significantly more efficient and seamless audit response.

In this session, we reviewed the administrative workflow and lifecycle of TIPS. Anticipating these milestones before the start of the project ensures greater predictability, enabling more strategic and efficient execution of your budget.